The Invesco Commodity Index Fund (DBC) is up 162% since COVID lows in April 2020. During the same period the MSCI World (ACWI) is only up 70%. Commodities have thus beaten stocks by 92% since April 2020 – consistent with my expectations at the time.

The reason for this strong commodity outperformance is largely two-fold. Fiscal stimulus provided by western governments – particularly the US government – was bigger than anything we have seen since World War II, and with the benefit of hindsight, too generous. It translated to consumers consuming fewer services due to COVID, but a lot more goods. Indeed, it is this surge in goods consumption that put unusual pressure on supply chains and increased the cost of transporting containers five-fold.

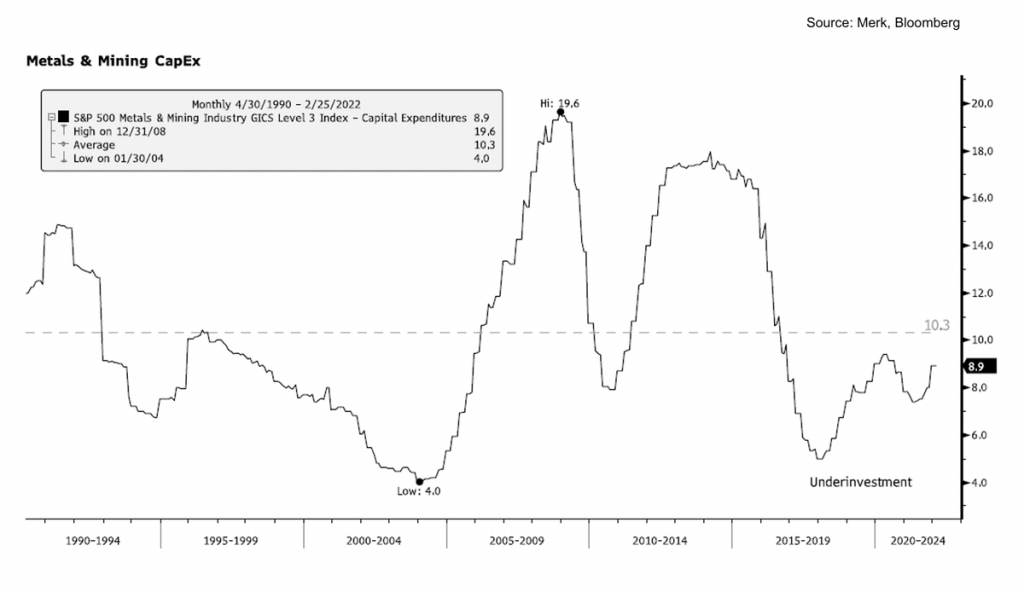

But a long period of underinvestment in new production capacity in several key commodities has also contributed to the quick rise, and will continue to be a dominant structural factor. Natural resources deplete. A conventional oil well has annual decline rates of a 4%-7% per year (while shale wells have much higher decline rates). Base and precious metals mines are often built and designed in a way to first mine the highest grade material in order to maximize returns. Without continued investment, production capacity of these assets declines. Growth in ESG investing (Environmental, Social, and Governance) was another factor that limited capital available to greenfield projects, be it in oil & gas or metallurgical coal. During a decade where technology outperformed every other sector (and resources underperformed), it was easy for investors and fund managers to write-off resources as the “old economy” and avoid it. Well, that is coming back to bite us now – in a huge way.

The War

By early 2022 the impact of COVID-related stimulus has started to wear off, and the short-term outlook was less clear, but Russia’s invasion of the Ukraine, changed the balance dramatically – very much in favor of commodities.

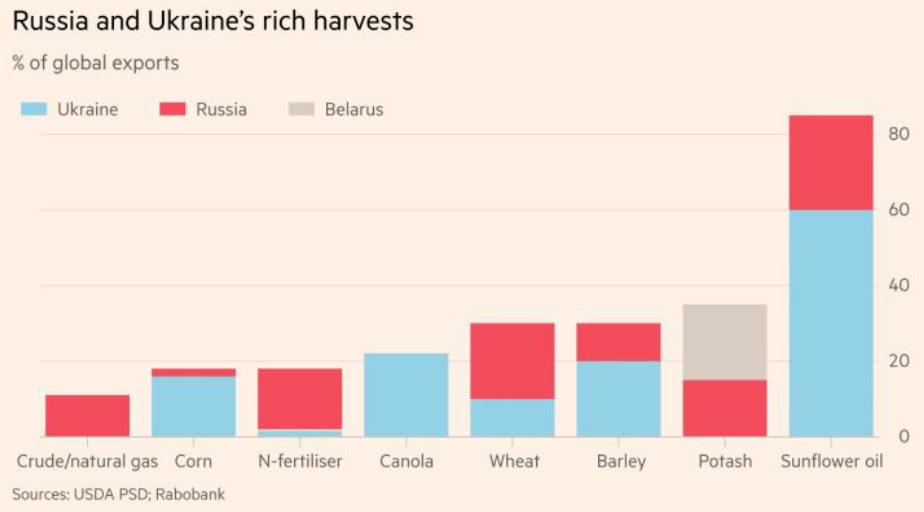

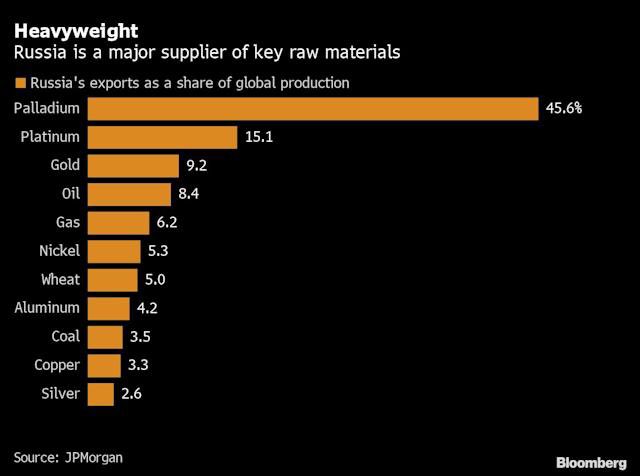

Russia, the Ukraine and Belarus are important exporters of commodities:

- Russia exported around 4.5 million of barrels of crude oil per day in 2020 – that’s 4.5% of world consumption and over 10% of exported oil (a lot of the oil produced is consumed domestically). The West would like to put an embargo on Russian oil, but even without an official embargo, most intermediaries don’t want to touch Russian oil.

- Russia and Ukraine accounted for 25% of global wheat exports – of which Russia alone for 18%. Obviously wheat and other grains will not get planted this season in the Ukraine. (at the same time Russia imports large amounts of seeds)

- Belarus accounted for 18% of global potash production (most of it exported), while Russia is a key exporter of ammonium nitrate, another essential fertilizer.

- Russia accounts for 10% of global aluminum exports, 20% of thermal coal exports and 12% of steel

- Russia is also a key producer of various other metals: vanadium, palladium and nickel – each of these is critical for certain applications

The war will have a real impact on commodity supply over the next 12 months, be it due to sanctions (which impact trade directly and indirectly), through SWIFT exclusion, due to direct war-related disruptions or even by Russia deciding unilaterally to limit certain exports.

Is it too late to buy?

I believe sanctions will persist for some time. Prices of key commodities are currently at historical highs, while valuation (even using trailing, much lower prices from 2021) are undemanding, resulting in very high cashflows relative to market caps. Risks to commodity prices remain two-sided in my opinion. Regardless of the war situation, the long-term underinvestment will not be resolved quickly. Demand destruction is the key factor to watch. Also not all names are created equal – some will prove more resilient with lower spot prices.

The dynamics in the commodity space are somewhat different from the other sectors (ie consumer, industrial). These characteristics make commodities so prone to booms and busts are.

1) Fixed Costs

Most commodity producers have a fixed cost of production. At least a large part of the cost is fixed. In mining diesel is often a significant cost, and we know that the cost of diesel is going up. So the costs are not completely fixed, but in the context of commodity prices surging by 100s of percent, they are roughly fixed.

By way of example, metallurgical coal producers’ (ie CRN AU or ARCH US) cost of production is around US$70/ton. In normal times they will sell their product at US$140/ton and make a respectable margin of 50% or $70/ton. The last quoted price for FOB Australian Coking Coal was over $600/ton. That’s closer to a 85% margin or over $500 per ton. At the same time, the trailing (CY 2021) EV/EBITDA is 4x for the sector (calendar year 2021 avg spot price was ~200/ton). Margins and cashflows will be off the charts as a percentage of market capitalization.

2) Inelastic Supply

A mine takes a long time to build – depending on the jurisdiction and other factors – but it’s often a 5-10 year time frame. On top of that ESG dissuaded majors from starting large greenfield projects (BHP and RIO no longer engage in coking coal). Oil and Gas also has long lead times (except shale). Over the past 6-7 years we’ve witnessed very significant underinvestment, and that will be felt in the subsequent years. Supply has no way of coming back quickly.

3) Inelastic demand

In shipping they say that 99 cargoes for 100 vessels make for a terrible market, while 100 cargoes for 99 vessels make for a booming market. It’s a similar dynamic in many commodities, which are essential for the functioning of our civilization. Most people will pay up to get the essential food, gas for heating, gasoline for transportation etc. Prices need to rise a lot for demand destruction to occur (most people won’t stop driving because gasoline price is up 50%). And there will be demand destruction (and of course substitution), but it will happen at higher prices and will of course be very painful. Think about the developing countries where food & energy are a large chunk of the consumption basket.

What to buy?

After a period of many lean years, we are now in a boom phase as the supply squeeze bites. I will discuss several names I currently hold (as of the time of writing). My positions can change anytime without written updates. This is not investment advice. Please do your own research before deciding to buy anything. Commodities are prone to booms and busts (as discussed above).

I have divided the portfolio into three buckets – energy, metals and mining and other. For each position I have provided a bloomberg ticker, a short description, the market capitalization (in USD) and my subjective risk assessment. The risk rating depends on whether the company is already generating revenues (or still building/developing the project), leverage to spot prices, balance sheet strength, and valuation. I believe all names on the list have substantial upside, but decided not to quantify it.

Energy Portfolio

Suncor (SU US or SU CN)

Suncor produces oil from Canadian oil sands at a cost of <$30/barrel and reserve life of 30+ years. The company also own significant storage, transportation and refining capacity in Canada. Trailing EV/EBTIDA to December 2020 is 6.0x. Management is splitting excess cashflows three-ways: debt reduction, dividend and share buybacks. The other two comparable names in this space are Canadian Natural Resources and Cenovus Energy.

Market cap: US$45.2bn (US$31.47)

Risk: low

Africa Oil (AOI CN)

Africa Oil is a Lundin family entity (Swedish family, active in natural resources) and their main producing asset is deepwater Nigeria with very low lifting costs (<$10/barrel), production runs at ~30k bopd. Only based on this asset, valuation is around 2x EV/EBITDA, while the market is attributing no value to the remaining assets: onshore Kenya (South Lokichar), offshore South Africa and its investee companies (Africa Energy, and Eco Atlantic). Most of its 2022 production from Nigeria has been hedged in the $70s, so will not benefit from the current rise in prices. There are no hedges thereafter.

Market cap: US$902m (C$2.50)

Risk: medium

More info: https://leadedlode.substack.com/p/africa-oil-corporationactivist-opportunity

Golar LNG (GLNG US)

Golar is an LNG business which will benefit from growth in LNG transport and infrastructure. It has simplified its corporate structure over the past year – it sold its Brazilian generation assets in exchange for New Fortress Energy shares (NFE – another interesting LNG infrastructure business) and floated its LNG carrier business (COOL in Oslo). It will now focus on FLNG – LNG infrastructure allowing to retrofit a LNG ship to liquefy and export natural gas, in particular from an offshore field. Current high gas prices in Europe/Asia create ideal conditions for a firm like Golar.

Market cap: US$2.0bn ($17.98)

Risk: medium

More info: http://philosophycap.com/research/GLNG.pdf

International Petroleum Co (IPCO SS or IPCO CN)

This is another Lundin company, which produces ~47k barrels of crude oil per day out of Canada (as well as smaller quantities in Malaysia). Very successful deleveraging over the past year. The company has no hedging and should fully benefit from the recent price spike. It is also in the midst of a 10.8 million share repurchase program.

Market cap: US$1.3bn (SEK 77.85)

Risk: high

TGS Nopec (TGS NO)

TGS provides seismic surveys of the seabed to oil & gas exploration companies. It is asset-light and does not own any equipment (the actual survey work is outsourced), but retains ownership of the data, which they can resell subsequently to other clients. Most cashflow gets paid out as dividends. An upturn is coming as much more producers’ cashflow will go towards exploration and TGS will benefit.

Market cap: US$1.4bn (NOK 122)

Risk: low

More info: https://www.gurufocus.com/news/1088992/read

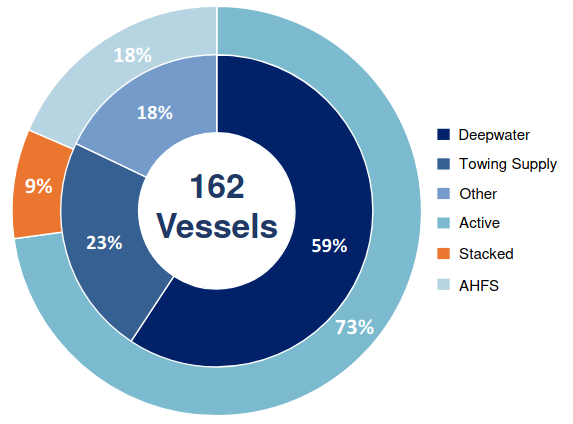

Tidewater (TDW US)

TDW owns offshore support vessels (OSVs). There were way too many OSVs after the last oil boom (2007-2014), which lead to a series of bankruptcies in the sector (TDW itself is post-restructuring). The sector has a healthier supply/demand balance today, which is likely to tighten in the coming quarters. Tidewater has been focusing on higher quality assets, and selling off older ones. The company is debt free and in 2021 was broadly free cashflow neutral.

Market cap: US$680m ($16.50)

Risk: medium

Hunting PLC (HTG LN)

HTG is a London-listed oil services company providing tools and components (consumables products, shale casing, drilling intervention tools) to upstream oil and gas industry. US shale is the single most important driver, however practically all major regions O&G producing regions buy from Hunting – by way of example Exxon put in a big order for titanium joints for Guyana last year. Military and aerospace are another source of revenue. HTG are similar to US-listed NOV and will benefit from the increase in CAPEX in the Americas. Russian pipe supply (ie from TMK group) to the oil & gas industry is largely going away with sanctions, which should benefit this company. HTG have no debt and a strong management team with a good track record.

Market cap: US$490m (GBp 246)

Risk: medium

Transocean (RIG US)

Transocean owns drilling rigs, that it leases. Day rates have been low for several years, but with the pick up in exploration and production activity offshore, there is a high probability of day rates rising in the coming quarters. Unlike its peers (VAL, NE) RIG has not restructured its debt during the lean years, and still has considerable financial leverage (US$6.7bn as o Dec-2021). Leverage obviously works both ways – in a strong market it should handsomely outperform its peers.

Market cap: US$2.8bn (US$4.24)

Risk: high

More info: https://beached.substack.com/p/transocean-rig-long-equity

Petrofac (PFC LN)

Petrofac is a bombed out oil & gas engineering firm. The firm has been the subject of an SFO (Serious Fraud Office) investigation in the UK, but the corruption case is now closed. There should be a lot of work for companies like PFC, while competition has mostly disappeared or shrunk over the last several lean years.

Market cap: US$680m (GBp 98)

Risk: medium

Metals & Mining Portfolio

Sprott Physical Uranium (U-U CN)

This is a fund that holds physical uranium in the Americas. I haven’t discussed uranium here, but the investment thesis has been discussed frequently in other places. There is also a vibrant Uranium twitter community. If it’s your first steps in this space, and you just want one account to follow, I can suggest @Big_U_Dawg

Market cap: US2.2bn (C$16.31)

Risk: low

Arch Coal (ARCH US)

ARCH finished construction of its second met coal mine Leer South in 2021, and the increased production of 8-9M tons from its US-based mines will benefit from the current record high pricing. The payback time for the investment in the new mine should be around 12 months. This year production will be backloaded (Q1 1.4Mt, Q2-Q4 2.5Mt). ARCH also have legacy thermal coal assets. These assets were not long ago seen as a liability, but with natural gas prices, thermal coal has also been very profitable. It remains the plan however to dispose of these. The company will relaunch a capital return program in Q2 2022 looking to return 50% of discretionary cash flow via dividends, while some of the remainder might also be used for share repurchases.

Market cap: US$2.3bn ($152.00)

Risk: medium

More info: https://twebs.substack.com/p/arch-spaces-prep

Coronado Resources (CRN AU)

Met coal miner with a great asset base split between Queensland (Curragh mine) and the US (Buchanan mine). In 2021 production was 17.4m tons at $66/ton. No debt, net cash.

Market cap: US$2.5bn (A$2.06)

Risk: medium

Bushveld Minerals (BMN LN)

Bushveld is a vanadium producer in South Africa. It’s only one of the four regions who produce significant amount of vanadium in the world (the others being China, Russia and Brazil). Vanadium is key ingredient in strengthening steel (still a growth market), and there is potential for additional use in vanadium redox flow batteries.

Market cap: US$198m (GBp 11.90)

Risk: high

More info: https://threadreaderapp.com/thread/1499302672574427136.html

Allegiance Coal (AHQ AU)

AHQ is listed in Australia, but holds its assets in Colorado (US), where it produces metalurgical coal from two mines (New Elk and Black Warrior), and has potential to increase production beyond the current 1.2m ton run-rate production. There is more upside in AHQ (vs ARCH/CRN discussed above), but probably also more risk as the company is still in the ramp up stage.

Market cap: US$150m (A$0.54)

Risk: high

More info: https://www.youtube.com/watch?v=FL5c_ioDwis

Whitehaven Coal (WHC AU)

WHC own a thermal coal mine in New South Wales, in Australia. As much as the world would like to move away from coal power generation, the reality is that in Asia, considerable electric generation capacity still operates on this dirty fuel, and will continue to do so. In calendar year 2021 Newcastle coal averaged US$125/ton and on that basis the company is valued at 4x EV/EBITDA. Current spot price however has exceeded $400/ton. The company is debt-free at this point, has started a share buyback (A$400m, up to 10% of outstanding shares) and reinstated a dividend.

Market cap: US$3.1bn (A$4.18)

Risk: medium

Geodrill (GEO CN)

This company provides drilling services to gold mining companies in Western Africa and Egypt. It’s well-run by founder/CEO, sports leading margins in its industry, an undemanding valuation of 3x EV/EBITDA (half of its peer group). Revenue has grown 40% YoY in 2021, while rig count grew 20% CAGR since inception. GEO has signed US$130m of long-term contracts for the first time recently and is planning to generate 60% from such contracts going forward.

Market cap: US$95m (C$2.76)

Risk: low

More info: https://seekingalpha.com/article/4375509-geodrill-selling-shovels-in-gold-rush

Equinox (EQX US / EQX CN)

EQX is my favorite gold mining play. They own six mines in the Americas (Brazil, Mexico, US and Canada). Four of which are currently producing (700k ounces/year), while the remaining two mines will be developed over the next 2-3 years. The objective is to hit 1m ounces of annual production by 2024/2025. Assuming delivery goes to plan, EQX will be the fastest growing large gold miner in the coming years. Management is top notch, in particular the chairman – Ross Beatty – is a legend in mining. He has been adding shares in January this year around $7.4/shr.

Market cap: US$2.4bn (US$7.84)

Risk: medium

Northern Star Resources (NST AU)

NST is a large gold producer (1.6m ounces/year) out of Western Australia. They have merged with Saracen in February 2021, which should bring out synergies given adjacent properties in the Kalgoorlie district. The company has a good track record of value creation and a strong management team.

Market cap: US$9bn (A$10.74)

Risk: low

Calidus Rsrcs (CAI AU)

Calidus will complete the construction of a mine in northern Western Australia, and will pour first gold in Q2 2022, with expected production expected at 90k ounces in the first year and rising slightly afterwards. 125k ounces have been hedged around US$1’700/ounce and the company will have debt of ~A$110m.

Market cap: US$230m (A$0.79)

Risk: medium

Serabi Gold (SRB LN)

Serabi is a small cap gold producer and explorer in Brazil. It has produced 34k ounces of gold in 2021, but is aiming (hoping?) for 100k ounces mid-term.

Market cap: US$52m (GBp 52.50)

Risk: high

Kodiak Copper (KDK CN)

KDK is a junior copper miner, who has already made a significant discovery of a copper porhyry system in British Colombia. It’s backed by Chris Taylor of Great Bear Resources – a very succesful gold explorer.

Market Cap: US$59m (C$1.55)

Risk: high

Rio2 Ltd (RIO CN)

Rio2 is a fully funded gold mine in northern Chile. Initial production is planned for 2022 at 100k ounces/year, but there is potential for further subsequent expansion. Alex Black and team have a great track record in building mines, and will make this one happen as well.

Market cap: US$ 147m (C$0.76)

Risk: high

Other

United Plantations (UPL MK)

UPL are one of the most efficient and environmentally friendly producers of palm oil in the world. In part this is due to their infrastructure: 530km of light railway to deliver fruit bunches to the mill and its ownership of a refinery. The company is controlled by the Danish-Malaysian Nielsen family. The company uses hedging to smooth the impact of price changes. In 2021 the realized palm oil (CPO) price was 3’309 MYR (Malaysian Ringgit) per ton, while the current spot price is >7’000 MYR.

Market cap: US$1.6bn (15.96 MYR)

Risk: low

More info: https://www.asiancenturystocks.com/p/deep-dive-2021-10-united-plantations

Comments?

Feel free to ping me on Twitter for any comments or suggestions.